Open trading account

Open trading account

Full report is available here.

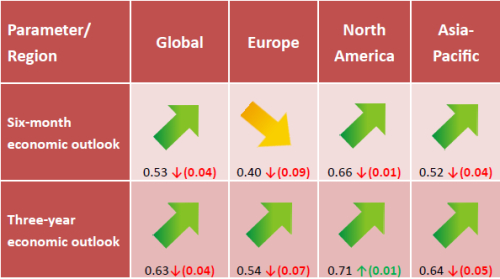

- The global economy expanded at its slowest pace in nearly three years in the first quarter of 2016 as a result of less resilient financial conditions mainly in the emerging markets, while the growth in the developed countries also remained sluggish. The major headwinds determining the global economic scene last month were the Fed’s rate hike expectations, latest updates from Chinese officials, indications that Japanese government and the BoJ could introduce further fiscal and monetary easing in the months to come and a steady rise in commodity prices. In the wake of these developments, professors’ sentiment seems to have run out of steam over the observed month.

- Rising nationalistic political moods around the Euro area along with a number of other economic challenges including worries about Britain’s potential exit from the European Union and uncertainty over the ‘Grexit’ saga seem to have somewhat shaken economists’ confidence in the bloc, while important growth indicators signaled a rather slow recovery, with the composite PMI hitting an over-one-year low in the observed month. The latter has sent both short and long term sentiment gauges significantly lower in May.

- While the Federal Reserve maintained a more hawkish stance, eyeing a summer rate hike on the back of incontrovertibly strong private consumption, North America still saw mixed results in May, as the six-month sentiment inched down slightly, while the three-year measure proved to continue its positive trend.

- The Asia-Pacific region kept performing below its potential during the prior month, with lingering domestic and external challenges putting a dent on the overall economic growth, as both short- and long-run sentiment indices slipped in the measured month.